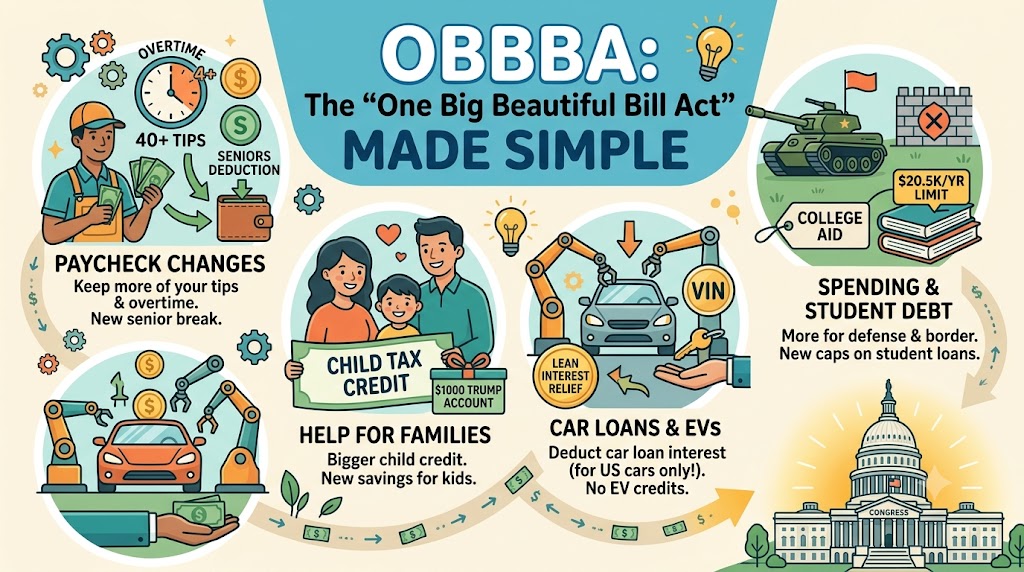

The U.S. government passed a massive law officially called the One Big Beautiful Bill Act, or OBBBA. Signed into law in July 2025, it is a giant package of rules about how the government spends money and how everyday people pay taxes.

Because the law is so big, it uses a lot of confusing language. Here is a breakdown of what the OBBBA actually does, explained in the simplest way based on what I researched.

1. Changes to Your Paycheck and Income

The OBBBA changes how the money you earn is taxed. Here are the biggest parts you will notice:

- No Tax on Overtime (Up to a Limit): If you work hourly and get paid extra for working more than 40 hours a week, you get a break. You can subtract your extra overtime earnings from your taxes up to $12,500 (or up to $25,000 for married couples filing jointly). However, this benefit completely phases out for individuals making over $150,000 (or $300,000 for joint filers).

- No Tax on Tips: If you work a job where you regularly earn tips, you can deduct that tip money from your income up to a maximum of $25,000 per year. There are a couple of catches: you must file a joint return if you’re married, and this deduction isn’t available to high earners making over $150,000 ($300,000 for joint filers) or anyone working in a Specified Service Trade or Business (SSTB).

- A New Break for Seniors: If you are age 65 or older, you can claim a brand-new, extra tax deduction of $6,000 (or $12,000 for a married couple if both qualify). This is on top of the standard deduction seniors already get. It begins to phase out if your income goes over $75,000 ($150,000 for joint filers).

- Permanent Lower Tax Rates: A few years ago, the government lowered tax rates for most Americans, but that deal was supposed to end soon. This new law makes those lower rates permanent.

2. Help for Families and Kids

The law includes several new rules aimed at helping parents save money.

- A Bigger Child Tax Credit: A “tax credit” is like a coupon that lowers your final tax bill dollar-for-dollar. The law raised this credit from $2,000 to $2,200 per child.

- Trump Accounts: This is a brand-new kind of savings account for kids under 18. For babies born between 2025 and 2028, the government will put a one-time $1,000 gift into the account to help them start saving. Parents and jobs can also add money to it over time.

3. Car Loans and Electric Vehicles

If you are planning to buy a car, the OBBBA changes the rules on what saves you money.

- Car Loan Interest Relief: If you take out a loan to buy a car, you can now subtract the interest you pay on that loan from your taxes (up to $10,000). But there is a catch: the car must be assembled in the United States.

- Goodbye, EV Tax Credits: The law completely ended the old tax breaks people used to get for buying electric vehicles (EVs).

4. Where the Government is Spending Money

The law did not just change taxes; it also shifted where the government spends its cash.

- More Money for Defense and the Border: The law adds $150 billion for military defense and another $150 billion for border security and immigration enforcement.

- Cuts to Medicaid and Food Help: To balance out the spending, the law cuts funding for Medicaid (health care for low-income families). It also adds stricter rules for people who get SNAP benefits (what many people call food stamps), meaning more adults will have to prove they are working to get food aid.

5. College, Graduate Students, and Alums

The OBBBA brings some of the biggest changes to federal student loans and college financial aid in decades. If you are in school now, planning to go later, or already paying off your debt, these new rules directly affect your wallet.

For Current and Future Undergraduate Students

- Part-Time Students Get Less Loan Money: If you take classes part-time instead of full-time, the government will now shrink the amount of federal student loan money you can borrow for that semester. Your loan size will match how many credits you take.

- Strict Caps on Parents: If your parents take out a federal loan to help pay for your school (called a Parent PLUS Loan), there is now a hard limit. Parents cannot borrow more than $20,000 per year, or more than $65,000 total over your entire college career.

For Current and Future Graduate Students

- No More “Grad PLUS” Loans: The government completely ended the Graduate PLUS loan program for new borrowers.

- New Borrowing Limits: Because Grad PLUS loans are gone, graduate students face strict limits on federal borrowing. You can only borrow up to $20,500 a year, with a total lifetime limit of $100,000 for graduate school. (If you are studying for a professional degree, like medical or law school, your yearly limit is $50,000, and your total limit is $200,000).

For Alums (Graduates with Existing Student Debt)

- New Repayment Options: Old income-based payment plans are being phased out. The government is replacing them with two main choices: the Tiered Standard Plan (a fixed monthly amount) or the brand-new Repayment Assistance Plan (RAP).

- How the RAP Plan Works: Your monthly payment is based entirely on how much money you make. If you make less than $10,000 a year, you only pay $10 a month. As your salary goes up, your payment becomes a specific percentage of your income (maxing out at 10% if you make over $100,000).

- The Catch for Forgiveness: Any leftover loan balance is forgiven after 30 years of payments. This is longer than some older plans, which offered forgiveness after 20 or 25 years.

- Fewer Safety Nets: If you lose your job or face an emergency, the old rules that allowed you to pause your payments for “unemployment” or “economic hardship” are gone. Instead, you can only pause your payments (called forbearance) for a maximum of 9 months every 2 years.

Key Terms to Remember

- Undergraduate Student: A college student working toward a two-year associate degree or a four-year bachelor’s degree.

- Graduate Student: A student who already graduated college and is working toward a master’s degree or a PhD.

- Professional Student: A student in a specific advanced program to train for a career like a doctor, lawyer, or dentist.

- Alum / Alumni: A person who has graduated from a school, college, or university.

- Tax Deduction: An amount of money you can subtract from your total income so you are taxed on a smaller number. (Like a discount before your tax is calculated).

- Tax Credit: A direct reduction of your final tax bill. If you owe $3,000 and have a $2,000 credit, you now only owe $1,000.

- Permanent: Lasting forever, or until a future Congress passes a new law to change it.

Where to Learn More (Easy-to-Read Sources)

- For Your Tax Questions (Tips, Overtime, Senior Breaks): Read the official IRS Fact Sheet on the OBBBA. While it is an official government page, it is broken down into short, bulleted lists that show the exact income limits and rules for cash tips, hourly overtime, and car loan interest.

- For Student Loans and College Financial Aid: Check the Federal Student Aid Office (FSA) website. This is the official government site for student debt, and it is widely recognized for using simple language, visual progress bars, and basic calculators to explain loan limits and repayment plans. (Note: You can look for their specific “OBBBA Changes” update page).

- To Check if a Car Qualifies for the Tax Break: Use the NHTSA VIN Decoder website. Your readers don’t need to understand manufacturing laws—they just type in their car’s 17-digit Vehicle Identification Number (VIN), and the site instantly tells them if the car was built in the United States.

- To Read the Actual Summary of the Law: Direct them to Congress.gov. While the full text of Public Law 119-21 is hundreds of pages long, the top of the page features a “Summary” tab written by independent researchers. It breaks the massive bill down into short, everyday paragraphs section by section, making it much less intimidating to read.

Stay educated, folks!

Leave a Reply